Community Forums › Forums › EA Studio › EA Studio Tools and Settings › EA Studio Tools and Settings: Experience and Results

Tagged: #acceptance criteria, EA Studio, FTMO-Data

- This topic has 286 replies, 38 voices, and was last updated 1 year, 6 months ago by

Alan Northam.

-

AuthorPosts

-

February 17, 2019 at 11:41 pm #9741

Petko Aleksandrov

ParticipantHey Viktor,

The R-squared is an update we have with EA Studio. It helps us generate strategies with better equity lines.

I have opened a topic in the Forum called EA Studio Updates – have a look at it, there is video and more details about R-squared.

February 18, 2019 at 10:47 pm #9755ParticipantR – squared is great improvement, I think it improved a lot the generator because it chooses more stable strategies

February 20, 2019 at 3:51 am #9779Roman

ParticipantMin Trades:200

R-Squared:75

OOS Stability:70%February 20, 2019 at 9:28 am #9784ParticipantAfter the video of Petko, I am planning to start using the OOS. It seems like really nice and useful. SImply, we do not use the whole period that we have but we use chosen % of Historical data. After that, we see the results that would have happened in the last months. And with the update int he acceptance criteria, we get only the good strategies.

February 20, 2019 at 9:30 am #9785ParticipantAnyway here is what I use:

Min count of trades 450

Profit factor 1.2

Max consecutive losses 7

Backtesting quality 99%

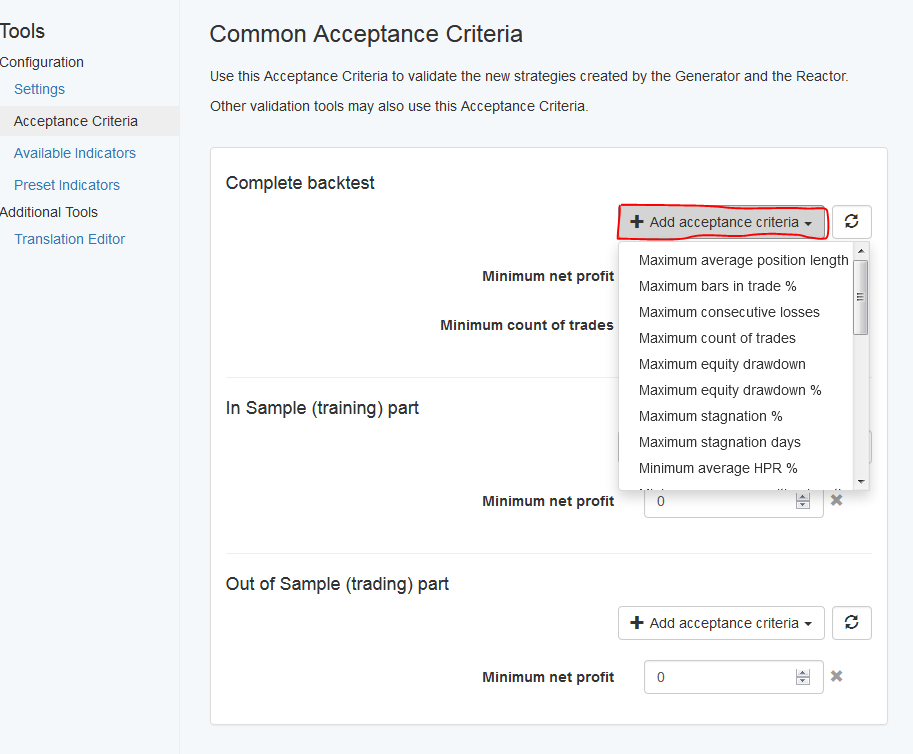

February 20, 2019 at 10:02 am #9790ParticipantHey Andi, you go it right, with the update of EA Studio acceptance criteria we can filter the separate sectors as In Sample and Out of Sample. That allows us to generate strategies that perform robustness tests as Multi Market and Monte Carlo in the In Sample part and in the same time those that pass the validation criteria in Out Of Sample part.

February 20, 2019 at 9:04 pm #9811ParticipantHola Andi! I’ve always used OOS, I was testing another software at the same time as FSB in 2017. With the search style they use OOS is very important. With it I still keep some of my data in my back pocket (about 3-6 months) just to really simulate and confirm simulated trading. This ensures at least for me the strategy has some strength I can depend on. Doing my method I may only find 1-5 strategies a day, but it helps me feel more secure with them. Even though we are testing on demo first, this keeps my demo free of clutter. Saves me time, space, and emotional excitement lol.

February 21, 2019 at 5:42 pm #9832ParticipantHey Roman,

you are very right here, OOS is very important, but once again the update now changed it a lot. We have the chance to choose acceptance criteria for the In Sample and for the Out Of Sample. Before it was for the complete backtest.

Personally, before the update, I did not use a lot the OOS. Simply because we were choosing the acceptance criteria for the complete backtest. So no matter what was OOS showing we were able to decide which strategy to use based on the whole test. Now we have it separately. This way we can choose what criteria to have in the generated part(In Sample), and what Training part(Out of Sample) to choose.

With simple words, now we really have the chance to simulate Demo trading with OOS.

March 8, 2019 at 12:01 am #10390ParticipantAs said I tested the OOS, and it worked just really great for me. The strategies are stable, they pass the robustness tests, and now I am on a nice profit on the Demo account, so I am sure that most of the EAs will go to my live trading portfolio.

Thanks, Petko! You really improve the systems and share with us! You are the man!

March 8, 2019 at 10:35 pm #10417Ossaio

ParticipantHi,

I’ve been generated strategies using FSB Pro but decided to check out EA Studio for the first time today. However, I’m encountering some issues and feel that I may have missed something very obvious.

Under Acceptance Criteria, I discovered that “Maximum Ambiguous Bars” is not available in the options. Was this removed?

Thanks.

March 8, 2019 at 11:23 pm #10419Participant

March 8, 2019 at 11:23 pm #10419ParticipantHey Ossaio,

Good topic here, I am sure it will be useful for many of the traders. The ambiguous bars were renamed to Minimum Backtest Quality. Keep it somewhere at 98-99.

Kind regards,

March 8, 2019 at 11:34 pm #10420ParticipantThank you very much Petko. It was indeed helpful!

March 8, 2019 at 11:54 pm #10422ParticipantCheers, Ossaio!

March 9, 2019 at 12:02 pm #10424ParticipantHey Andi,

I am glad to hear that my videos improved your Experts trading.

I follow along all updated with EA Studio and test them when I find the method that works the best for me, I will always share it.

Anyway, OOS is great to be combined with the acceptance criteria.

March 13, 2019 at 8:09 am #10518ParticipantIs there any correlation between the Minimum count of trades and Monte Carlo?

-

AuthorPosts

- You must be logged in to reply to this topic.