Community Forums › Forums › EA Studio › EA Studio Tools and Settings › EA Studio Tools and Settings: Experience and Results

Tagged: #acceptance criteria, EA Studio, FTMO-Data

- This topic has 286 replies, 38 voices, and was last updated 1 year, 6 months ago by

Alan Northam.

-

AuthorPosts

-

August 24, 2024 at 3:36 am #302352

Ricky Suen

ParticipantAlan, could you change the data horizon to 1 Nov 2023 – 31 Nov 2023 and recalculate the portfolio?

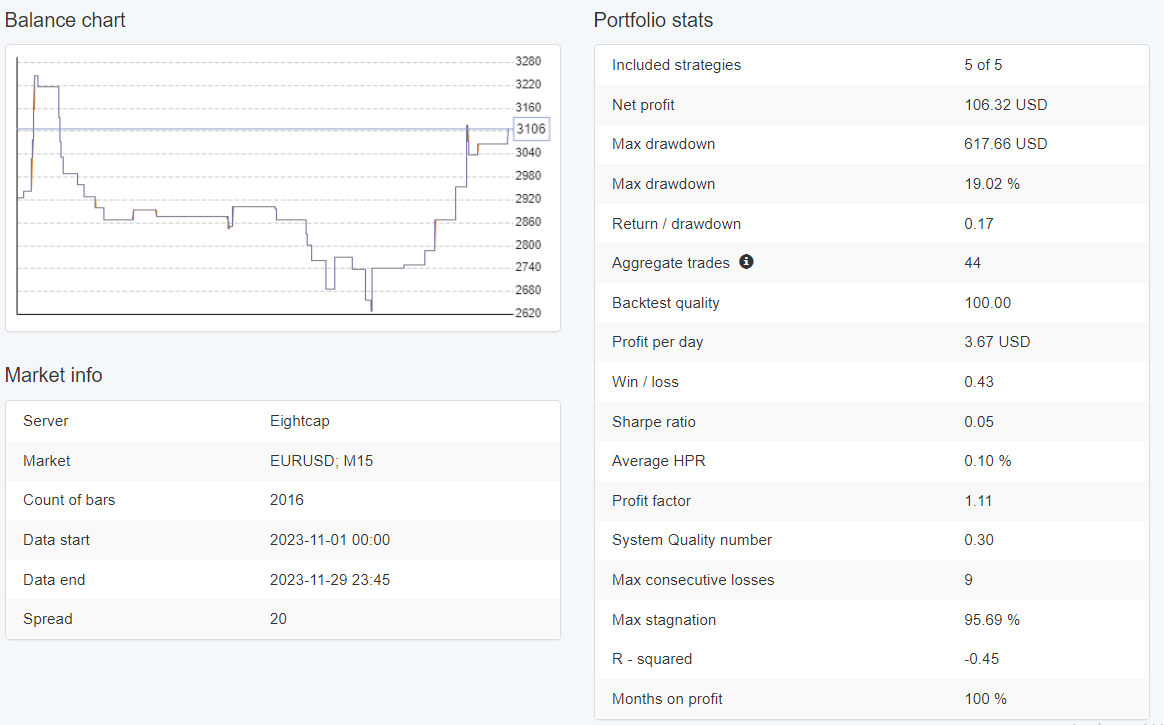

August 24, 2024 at 11:59 am #302396Alan Northam

ParticipantNovember only has 30 days so I set it to 30 Nov 2023 :o)

Here is Month of December

Here is link to my Dropbox where you can download the settings file:

Click on link, click on file, click on download

Alan,

August 24, 2024 at 12:53 pm #302413Participant August 24, 2024 at 12:55 pm #302414Participant

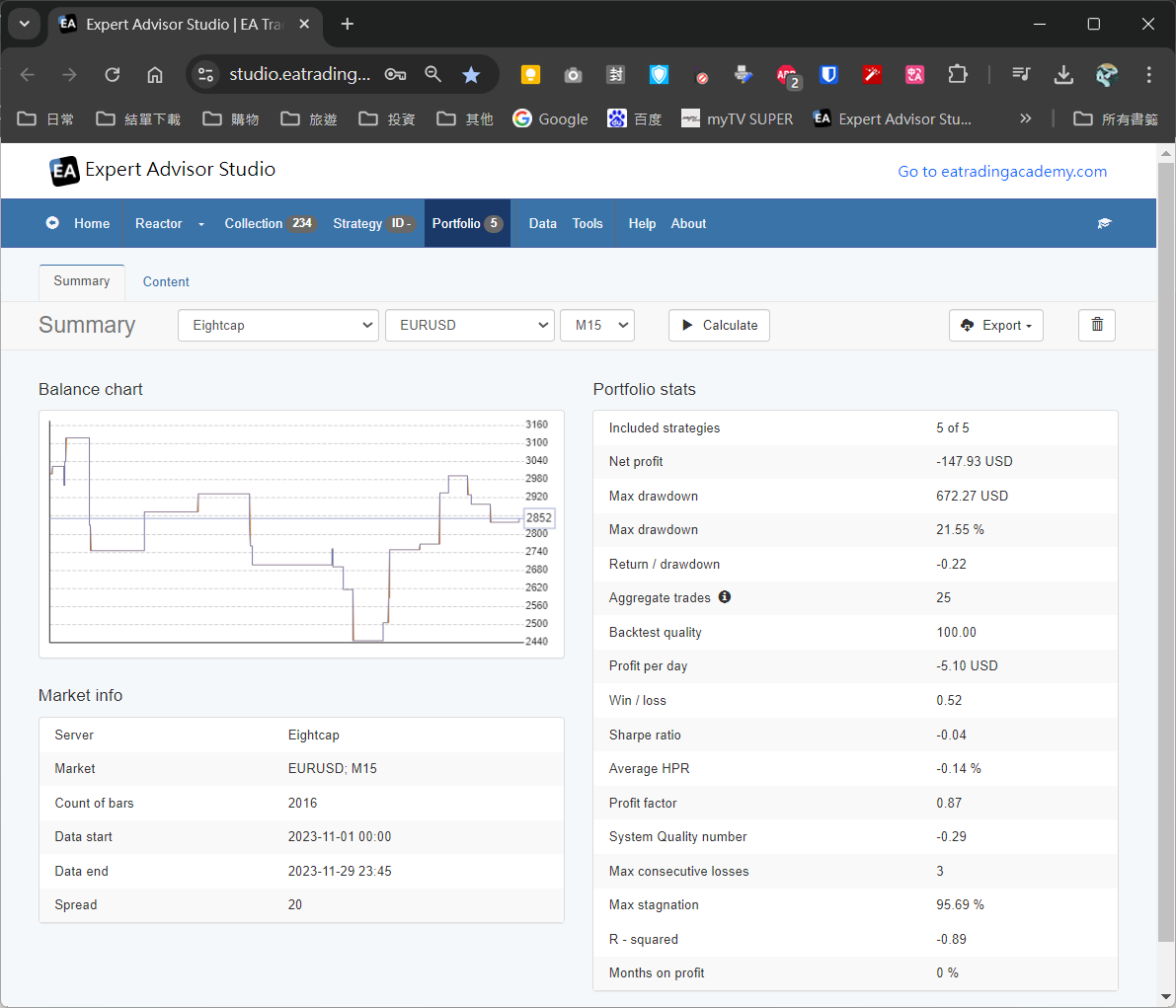

August 24, 2024 at 12:55 pm #302414ParticipantWhy did I still get negative result?

August 24, 2024 at 1:48 pm #302429ParticipantI will run the test again and see what I get.

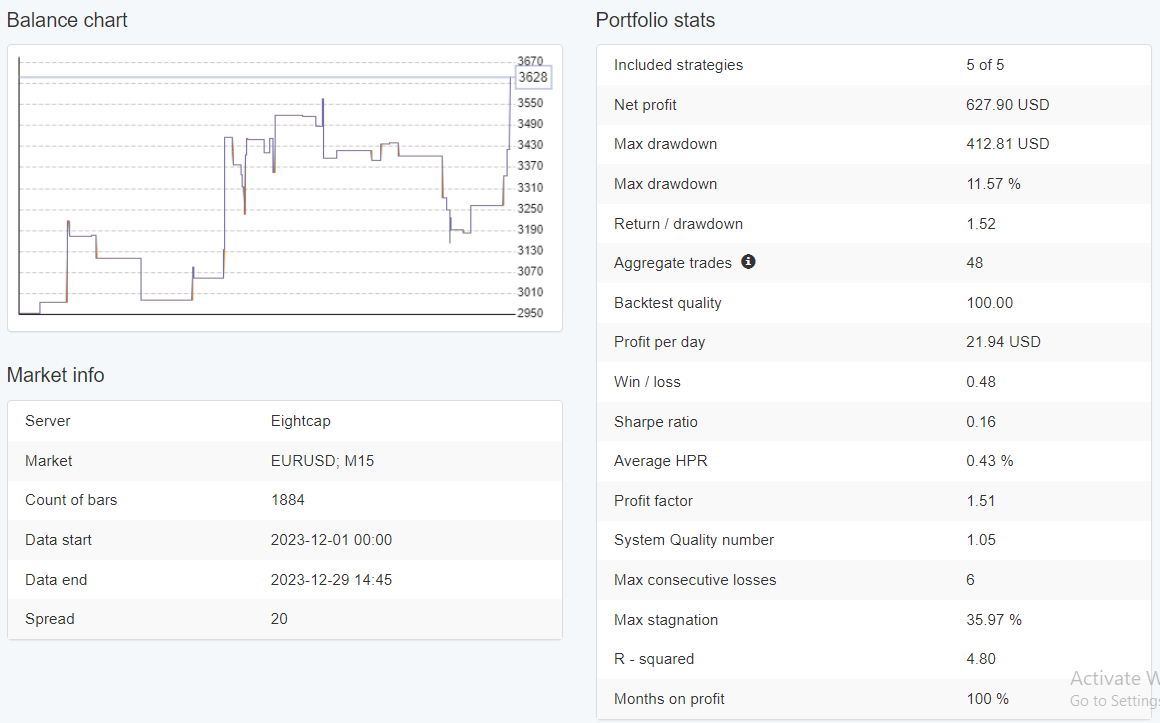

August 24, 2024 at 2:45 pm #302434ParticipantI see what I did. I collected the strategies using Blackbull and then somehow switched to Eightcap to select the top 5. When I do this again I get positive profit for the portfolio in November. However, if I use Eightcap to generate the strategies in the collection and then select the top 5 making sure I am still using Eightcap I do show a loss for the portfolio in November. I will have to start all over again. Sorry for the confusion!

Alan,

August 25, 2024 at 1:01 pm #302575ParticipantHi Ricky,

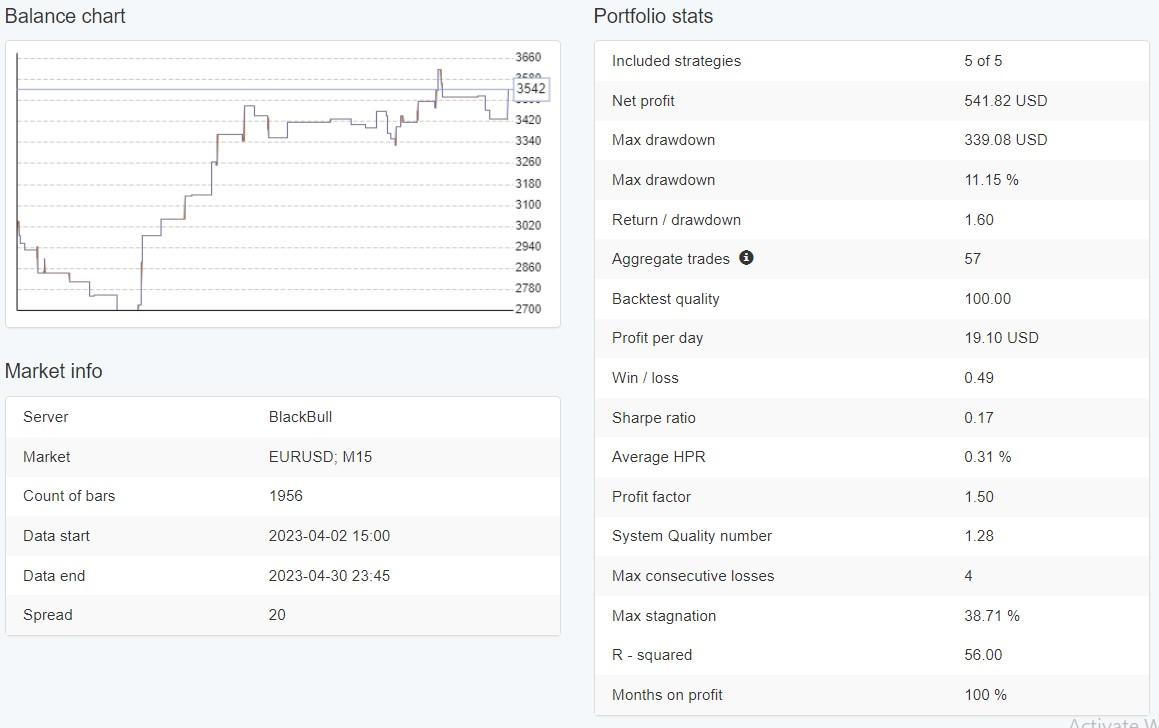

Yesterday I tried many times to generate strategies that would show profit in November 2023 but could not find any. I then sat out to determine why. I finally decided to look at the Indicator chart for EURUSD for the complete year of 2023. I found the date period of June 1, 2023 through October 31, 2023 to be mostly during the period in which EURUSD was trading in a range. So what happens is EA Studio then creates strategies that work good in trading ranges. However, the test period of the whole month of November was in a trending period of the market. The problem is strategies that are generated during trading ranges do not work well during the period of time when the markets are trending. I was able to find one or two strategy that did manage to show profit during the month of November but I could not find 5 or more strategies to add to a portfolio that would show profit during the month of November. I then generated strategies for the first 3 months of 2023, added the top 5 to a portfolio and then looked at how they performed during the month of April. During these four months the market was trending. I found the portfolio did result in nice profit during the month of April.

Note: I used OOS = 30% for January 1, 2023 through March 31, 2023 to have out of sample equal to one month.

Alan,

August 25, 2024 at 2:00 pm #302580ParticipantHi Ricky,

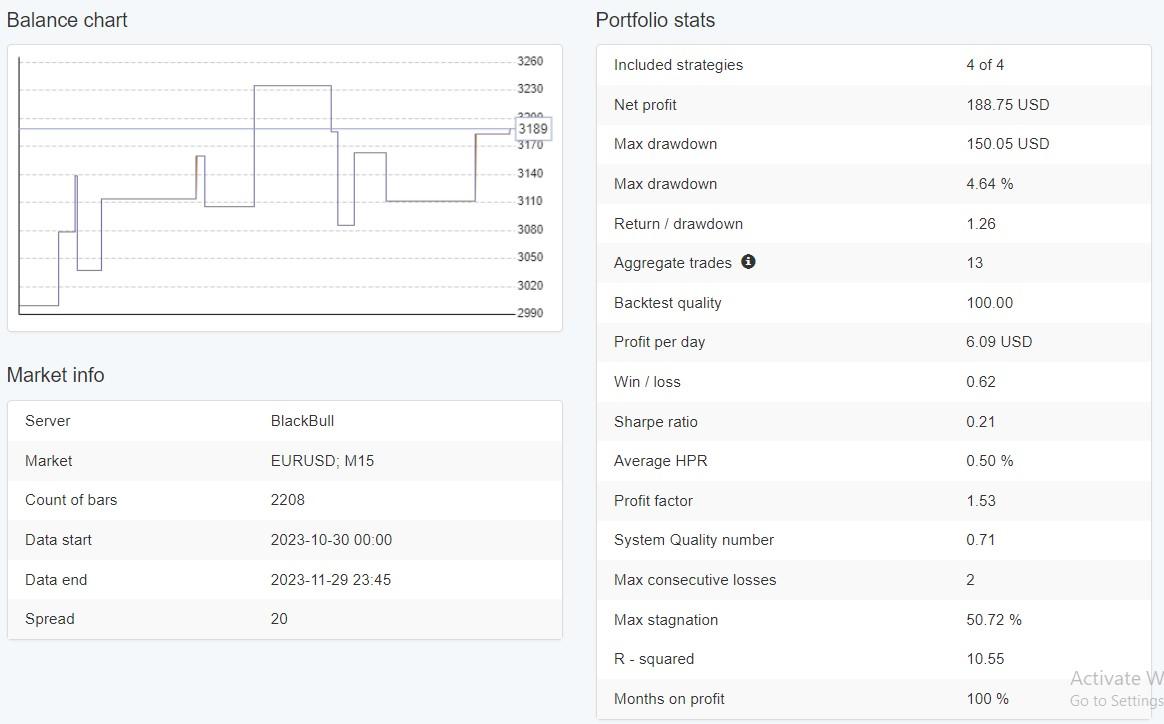

Finally what I did was to generate strategies from October 2018 through October 2023, 5 years for EURUSD. I set the OOS to 30% to see profit for last one year of trading. By using 5 years of data the indicators used have settings that generate profits over the long term which then includes many periods of trending and ranging periods. This is why Petko uses 5 years of historical data when generating strategies. I then looked at profits generated while trading during the month of November 2023. Results show a profit of $188.75 for the month of November 2023 with 13 trades.

What all this testing shows is when generating strategies you need to include multiple periods of trending and ranging markets to create strategies that will work well in future market conditions.

Also by using an OOS equal to one year shows how well the indicators work when actually trading over a future one year market conditions.

Alan,

If you are evaluating EA Studio and have not purchased it yet but has decided to purchase it please use this link to give me credit for your order. Thanks! Alan–

August 25, 2024 at 5:45 pm #302607ParticipantThank you for your effort, Alan. I am sorry that I have already bought the EA Studio so I can also give you a verbal credit here ;). If I do not misunderstand, you suggested my using a longer period for the training and applying the strategies in a longer period. Both of the training period and the trading period should contain trending durations and ranging durations. I will try this approach in my setup to examine the result. Thanks again.

August 25, 2024 at 9:39 pm #302636ParticipantHi Ricky,

You should use a longer period such as 3 to 5 years to generate strategies so as to cover multiple trending and ranging periods. In my opinion the OOS period should be longer than the future time frame you wish to trade before updating EAs. For example if your strategy is to update EAs on a weekly basis then make the OOS period at least 2 weeks. I would also suggest selecting strategies in the Collection that are moving upward on the right edge of their balance line charts. I also suggest using more entry and exit indicators so the strategies generated will execute better trades such as 4 entry indicators and 2 exit indicators. Experiment, try different combinations, see what works best for you.

Alan,

August 31, 2024 at 7:39 am #303508Participant

Sorry that I have taken a short trip so I cannot respond to your reply promptly.

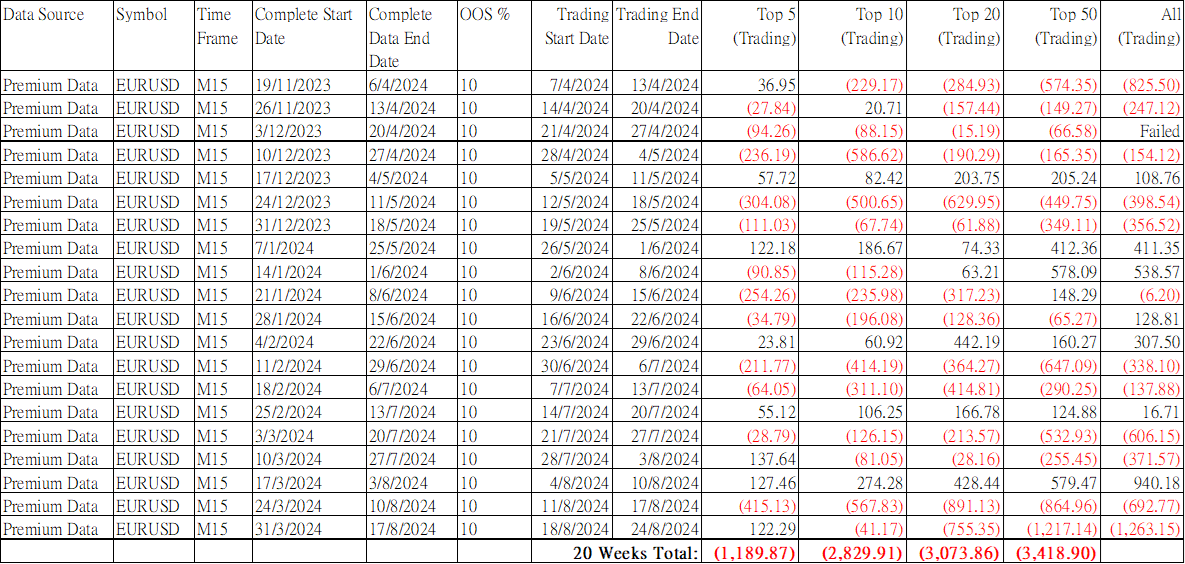

Nevertheless, I tried your suggestions and did an experiment. For the generator, I set the data horizon to 20 weeks and used 10% for the OOS which is about 2 weeks. The max entry indicators and max exit indicators are set to 4 and 2 respectively. For the round 1, I used the historical data of 19/11/2023 to 6/4/2024 (totally 20 weeks) to generate 100 strategies from EA Studio. Then I selected the top 5, top 10, top 20, top 50 and all strategies for trading in the next week. The results are recorded. The same process was then repeated 20 times for the subsequent weeks. The table posted above shown all the recorded results.

I cannot use 3 to 5 years for the generation because it will make the OOS period too long.

You can see that most of the trading results are still losing. May I know if you have any further suggestions to improve the result?

August 31, 2024 at 10:25 pm #303661ParticipantWhen using 20 weeks to generate strategies and then trading for only one week the losing weeks in your table may be a result of the market going through drawdowns. I would suggest increasing your trading time frame to one week, two weeks, and four weeks to see if results improve with longer trading time frames.

Also, generate strategies for 1 year with OOS 10% and then trade for one week, two weeks, and four weeks to see how trading improves with longer time frames.

Also, generate strategies for 2 years with OOS 10% and then trade for one week, two weeks, and four weeks to see how trading improves with longer time frames.

Also, generate strategies for 3 years, etc, with OOS 10% and then trade for one week, two weeks, and four weeks to see how trading improves with longer time frames.

Keep trying different combinations and eventually you will find what works best for you.

Alan,

September 1, 2024 at 6:31 am #303706ParticipantI understand that I can try all the combinations to see which ones are profitable. But I want to know if there is any before starting a full scale testing. My approach is just using the historical data to generate strategies and to use them in the next week or month. It is quite simple and straightforward. May I know if anyone had used this approach to get profit consistantly? If so, could you share the combinations they are using?

September 1, 2024 at 6:56 am #303708ParticipantI am also very curious why the result is so strange. If you generated a group of profitable strategies for the period 1 to period n, you expect that the group of strategies is also profitable in period n + 1. Or at least they are not losing. It seems that this assumption is not true. If the profitability of a strategy in the past is not related to the profitability in the future, what is the point to do backtesting?

September 2, 2024 at 7:43 am #303849Participant

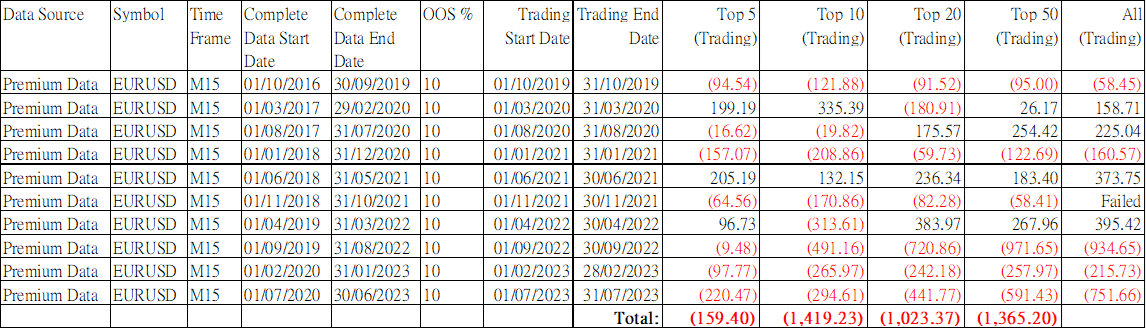

I did another experiment. According to your suggestion, I used 3 years of data for training, 10% OSS and the trading period is one month. To avoid focusing on one type of market condition, I spread the trading periods between 2019 to 2023. The trading periods are separated by 4 months. In addition, I added Monte Carlo simulation for the market variations to increase the robustness. The result is shown above.

It seems that the result has no improvement. Do you know what is going wrong?

-

AuthorPosts

- You must be logged in to reply to this topic.